Tommaso Di Francesco

About Me

I am a postdoctoral researcher in the Finance group of the Department of Economics at the University of Bonn. I hold a double PhD in Economics from the University of Amsterdam and Ca’ Foscari University of Venice.

Research Interests

Behavioral Macro and Financial models, with a particular interest in expectation formation and heterogeneous agent modelling.

I am trying to mantain a reading list of recent papers in topics that interest me. Find the March list in this

News

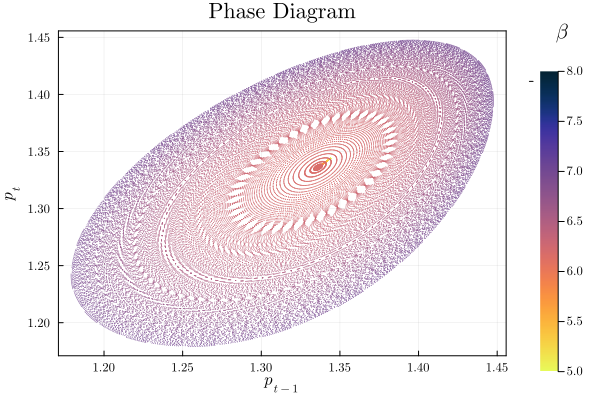

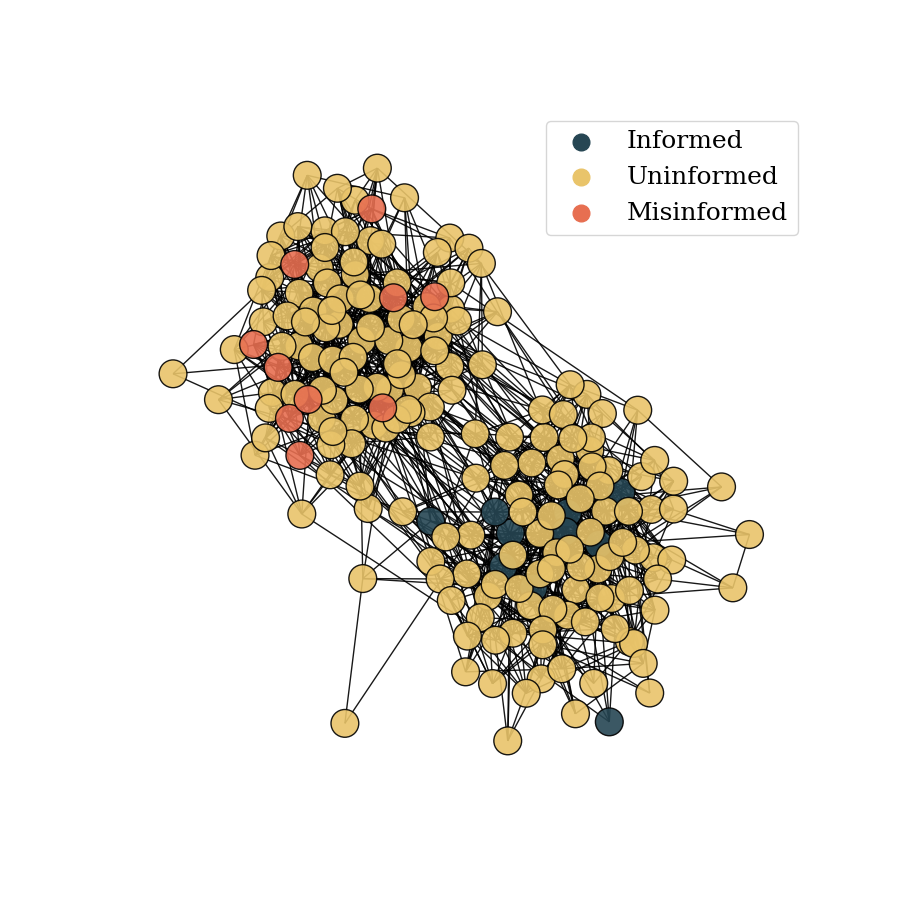

- [Oct. 2025] “(Mis)information Diffusion and the Financial Market” was published in the Journal of Economic Behavior & Organization!

- [Sep. 2025] Joining the Finance group at the University of Bonn as a Postdoctoral researcher!

Publications

-

JEDC

Journal of Economic Dynamics and Control, 2025.

JEDC

Journal of Economic Dynamics and Control, 2025. -

JEBO

Journal of Economic Behavior & Organization, 2025.

JEBO

Journal of Economic Behavior & Organization, 2025.

Work in Progress

-

Sticky Information across the Wealth Distribution

Tommaso Di Francesco — -

Sparse Learning and Endogenous Pockets of Predictability

Tommaso Di Francesco, Stafanie Huber, and Jonathan Seim —

Teaching

Teaching

Econometrics 2 — 2024/2025, University of Amsterdam Statistics — 2024/2025, University of Amsterdam Mathematics 1 for Economics — 2024/2025, University of Amsterdam Microeconomics for AE — 2024/2025, University of Amsterdam Optimization — 2019/2020, 2022/2023, University of Venice Financial Mathematics — 2019/2020, University of Venice Mathematics for Economics - 2019/2020, University of Venice

Powered by Jekyll and Minimal Light theme.